Engaging Advisors in Asset Recycling

Photo Credit: Image by Pixabay

On this page: Find details in engaging advisors for an asset recycling transaction. Read more below, or visit the Guidelines for Implementing Asset Recycling Transactions section and Content Outline, or Download the Full Report.

Advisors should be engaged for the preparation and bidding phases of an asset recycling transaction. The team of transaction advisors would typically consist of a lead transaction/financial advisor, supported by technical and legal advisors.

Other specialists such as environmental expert, social expert and insurance, accounting and tax advisors may also be appointed depending on the asset(s) and the transaction.

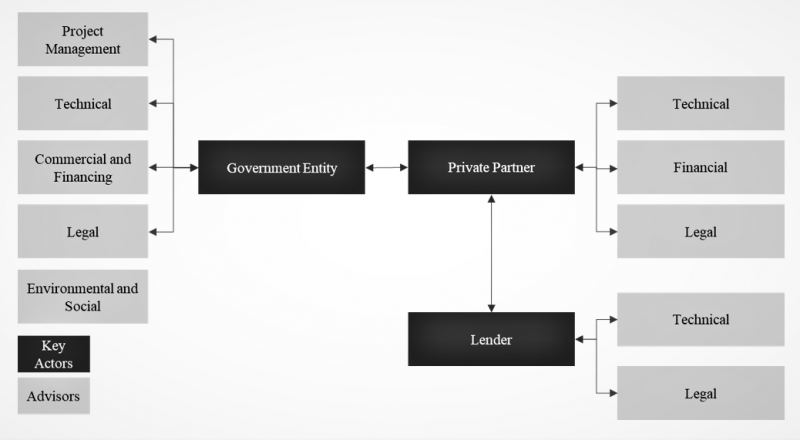

Figure 1: Advisory Services for an Asset Recycling Project The engagement of advisors should consider three considerations: (i) Setting up a coherent multidisciplinary team, (ii) ensuring independent advice and (iii) value for money in engaging the advisory services. Key aspects that should be considered are: Terms of reference should set out the context and objectives of the transaction, how the transaction is to be managed, the role of the advisor, and the required deliverables and deadlines. Scope of work should be clear, specific, and time-bound and should not be open-ended. The size requirements of the advisor's team over the transaction phases should be carefully considered. The team may need to scale up or down to adapt to the workload over the transaction phases. Asset-recycling and sectoral experience should be an important selection criterion and should be evidenced by a credible set of credentials. Evaluation should focus on the skills of the nominated individuals and the firm. The quality of an assignment depends on the quality of the people involved. The firm’s reputation and track-record of relevant mandates and the credentials of the individuals proposed should also be carefully considered. There should be sufficient flexibility to allow for contingencies such as extension of scope or time in delivering the transaction. In evaluating the potential advisers, the Relevant Authority should ensure a balanced approach in evaluation to ensure that sufficient consideration is given to the track record and ability of the adviser so that the lowest price proposition is not always favored. The Relevant Authority should determine if advisors should be engaged through an integrated contract or separate contracts. The decision must be taken case by case by considering (i) the local advisory market (ii) resources available within the Relevant Authority to manage the transaction and (iii) the features and complexity of the proposed transaction. Description of the procurement models are provided below: Integrated contract – A single procurement procedure is launched to appoint a consortium of advisors. This presents a more streamlined approach to the Relevant Authority; requiring less involvement in coordinating separate advisors and should have lower interface risks amongst the various advisors. The head or lead contractor will be responsible for coordinating the inputs and deliverables under such a contract. A disadvantage is that the Relevant Authority may not be able to engage the best advisor in each respective field as the consultancy team determines the make-up of the advisory team. This can be mitigated by Relevant Authority setting clear criteria and the skills required for selection and for each specific advisor. Separate contract – Procurement procedure is launched for each advisor required for the project. This will require the management of different sets of advisers if there is no project management firm or lead advisor appointed. Given separate contracting required, the procurement and the contracting processes may require more resources and time. A disadvantage is that Relevant Authority may not be able to leverage the synergies among the advisors. The government entity will need to not only manage various advisors, but also integrate advice from the separate workstreams. This may be the responsibility of the Relevant Authority, or it may need to appoint one of the advisors (typically the financial advisor) to do so (for a fee). Mixed – It is possible to use a mixed approach by mandating a separate contract for a specific advisor, for example where a specific workstream is very critical or where availability of good advisors seem rather limited and appoint the others as a consortium. The advisor’s terms of engagement should include (i) the phase covering due diligence, the preparation of business case and advising on the optimal asset recycling project structure, (ii) the procurement phase including the preparation of the tender documents, the running of the bid process and evaluation of bids, (iii) negotiations with the preferred bidder and up to contract and financial close, and (iv) preparation of contract management plan, including reporting requirements and training workshops for the Relevant Authority to build capacity on monitoring performance and contract administration. The fees should provide effective incentives for the advisors to meet the Relevant Authority’s objectives for the transaction. Advisors should be remunerated based on delivering the prescribed work packages that cover identifiable phases of the project’s development with remuneration commensurate with effort and complexity of the transaction. There should be some flexibility that allows the Relevant Authority to implement some changes in scope and extensions. The following key elements in drafting the terms of reference for the advisors should be considered: Table 2: Key Elements in Drafting Terms of Reference Lead Transaction Advisor/ Financial Advisor Assist Relevant Authority in the coordination of all advisors and manage interfaces between government officials and other advisors. Support development of the financial aspects of the transaction - appraisal of different transaction options, financial modelling, and inputs on bankability and financial advisory. Determine and develop the requirements for submitting a financial bid. Ensure that financial aspects of the bidders' solutions meet the requirements for submitting a financial bid. Review financial models submitted by bidders and advise of risks. Evaluate and advise on all financial proposals. Review the funding, accounting, and taxation aspects of solutions proposed by bidders to ensure deliverability. Undertake financial due diligence on bids submitted. Preparation of implementation guidelines to help the Relevant Authority operations team implement the transaction in accordance with the agreement. Identify and evaluate other sources of funding (including, project finance, climate finance, or Islamic finance) for the asset/ related projects or for use of proceeds resulting from the asset/ related projects. Technical Advisor Support the development of the technical aspects of the transaction; including scope of the private sector’s responsibility with respect to the asset. Draft the asset/transaction’s performance specifications (and if required any capital investment that may be required). Evaluate and advise on technical solutions over the tender phase; including matters relating to labour, maintenance regime and lifecycle renewal. Undertake technical due diligence on bidders' solutions particularly with respect to asset maintenance and operations, asset management and lifecycle refurbishments. Assess bidders’ technical proposal and advise on deliverability in terms of meeting proposed contracted performance requirements. Provide support in the clarification and refinement of technical issues with preferred bidder/s. Preparation of implementation guidelines to help Relevant Authority operations team monitor the project in accordance with the agreement. Legal Advisor Assist Relevant Authority in assessing the requisite powers and legal feasibility of the transaction. Develop the contract documentation for the transaction. Develop other legal aspects of bid documents, including analysis of the asset/s, land ownership, interface agreements, and other site-related issues. Identify all legal and regulatory approvals that would be required for the transaction and lead preparation of all documents required to support securing these approvals. Ensure that bids meet legal and contractual requirements. Evaluate and advise on all processes and legal and contractual solutions throughout the procurement phase and minimize the risk of bid challenge. Undertake legal due diligence on bids. Provide support in the clarification and fine-tuning of legal aspects of the transaction. Preparation of implementation guidelines to help the Relevant Authority operations team implement the project in accordance with the transaction agreements. Accounting / tax Advisor Provide advice with respect to tax and accounting implications of the transaction. Assess tax and accounting treatment of the transaction to the Relevant Authority and review any associated risks. Environmental and Climate Resilience Determine the GHG emissions baseline of the asset Assess bidders’ technical solutions proposed in terms of their impact on future GHG emission pathways and climate resilience enhancement. Identify climate-related risks, such as risks related to the physical impacts of climate change (Climate Change Physical Risks) and risks related to the transition to a lower-carbon economy (Climate Change Transition Risks) Identify opportunities for enhancing the asset to become a sustainable asset or opportunities to use the proceeds in green, social or sustainable projects.Advisory Services for an Asset Recycling Project

Selection of advisors

Structuring advisor’s contract

Optimum length of advisory contracts

Payment structure

Key Elements in Drafting Terms of Reference

Category

Scope / Terms of Reference

The Guidelines have not been prepared with any specific transaction in mind and are meant to serve only as general guidance. It is therefore critical that the Guidelines be reviewed and adapted for specific transactions To find more, visit the Guidelines to Implementing Asset Recycling Transactions Section Overview and Content Outline, or Download the Full Report.

![]()

Updated:

TABLE OF CONTENTS

I. GUIDELINES FOR IMPLEMENTING ASSET RECYCLING

3. Guidelines for Asset Identification

• Engaging Advisors in Asset Recycling

• Due Diligence Process in Asset Recycling

• Guidelines for Legal and Commercial Structuring Options

• Market Sounding in Asset Recycling

Related Content

Additional Resources

Sample TORs by Project

Type of ResourceAppointing and Managing Advisors

Type of Resource