Classification of Emissions Reduction Credit

Photo Credit: Image by Freepik

On this page: ERC classification is relevant for how the units are transacted. Read more below, or visit Strategic Guidance for Country System Assessments, Guidance for Countries in Assessing ERC Projects, or Mobilizing ERC Finance.

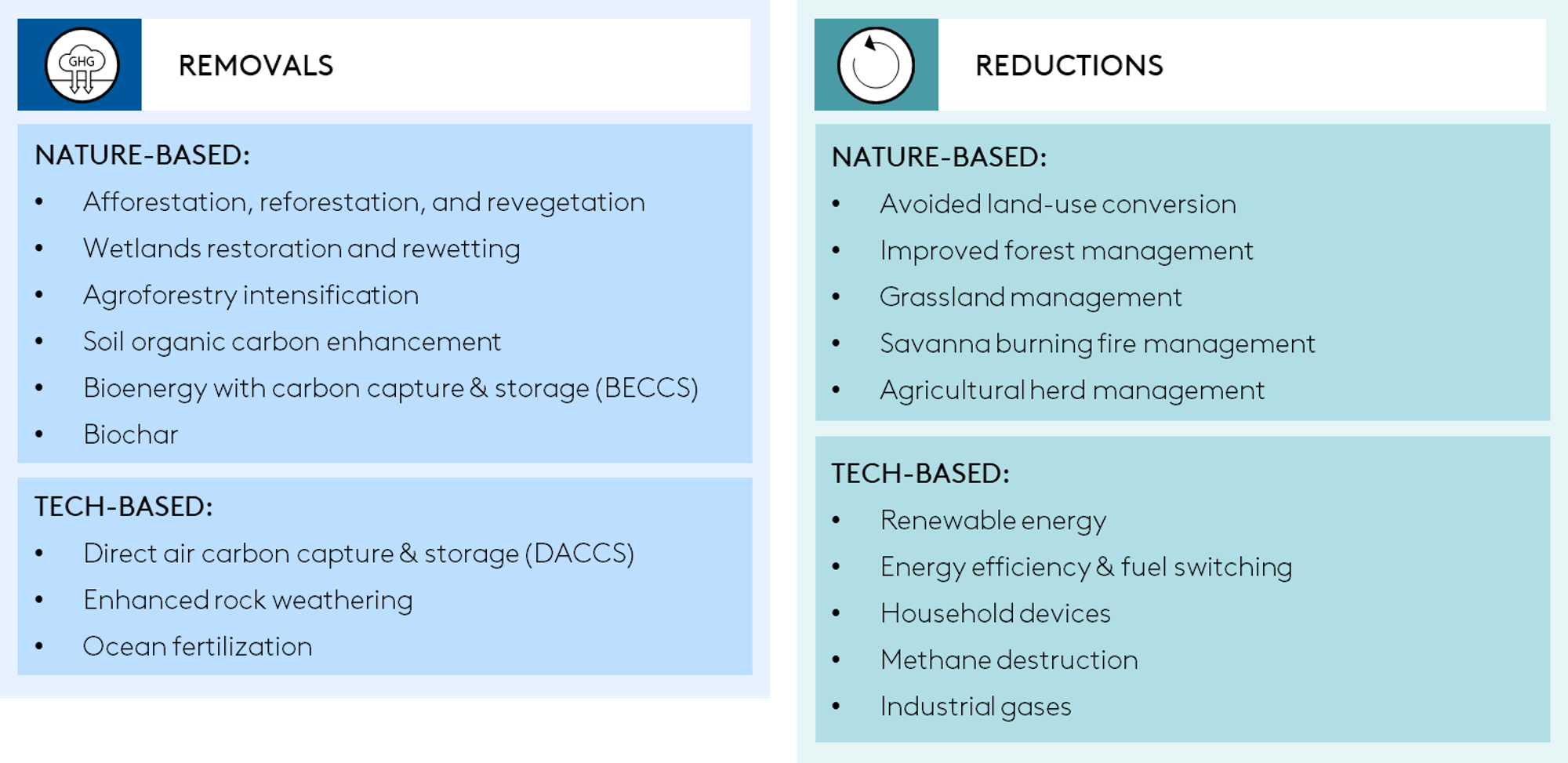

An emissions reduction credit (ERC) is a discrete unit which represents a specific amount of greenhouse gas (GHG) emissions reduced or removed, representing one tonne of carbon dioxide equivalent tCO2e. ‘ERC’ is often used interchangeably with ‘carbon credit,’ and can be used to describe credits generated and purchased for a variety of purposes, including voluntary use and domestic and international compliance. To ensure their uniqueness and for the purpose of avoiding double counting, ERCs are issued, tracked, and cancelled on central registries which are maintained by regulated compliance programs and voluntary crediting schemes. These registries often assign each ERC with a serial number for unique identification. ERCs can be classified by their crediting mechanism through which they are supplied and market segment characterizing where they are purchased (Figure 1) and by the ERC activity (Figure 2). ERC classification is relevant for how the units are transacted. For example, ERCs used for compliance purposes will need to meet the requirements set forth in the compliance program while ERCs used for voluntary purposes will need to meet the standard’s requirements as well as buyer preferences for certain characteristics (e.g., project type). Figure 1: Types of carbon crediting mechanisms (supply) and market segments (demand).1 Figure 2: Illustrative representation of ERC classifications by example activity types (non-exhaustive). table 1: Key ERC-related terms Additionality Emissions reductions or removals are additional if the mitigation outcomes were only made possible by the carbon credit-generating activity. For example, emissions reductions or removals would be considered nonadditional if the mitigation outcomes underlying the carbon credits would have been achieved under enforced policy requirements or common practices. Article 6 Article 6 of the Paris Agreement provides the overarching global framework for international cooperation through market-based and non-market-based measures for climate mitigation and adaptation. Carbon crediting program A scheme (voluntary or compliance-based) managed by a central organization that registers climate change mitigation activities and issues carbon credits for the ERs achieved by those activities. Co-benefits Non-carbon benefits arising from the mitigation activities which have positive social and environmental impacts. Corresponding adjustment An accounting method to be applied to ITMOs within the context of Article 6 of the Paris Agreement to avoid double counting. In practice, a country that authorizes the transfer of mitigation outcomes to a purchaser makes an addition to its account of emissions and the country acquiring and using the ITMOs toward its NDC makes a subtraction. A corresponding adjustment is used to ensure that the host country does not use the volume of ERs (which forms the basis of the ITMOs being sold to a third party) for its own NDC achievement, which would constitute double counting. As of the date of this report, host countries may decide whether and when to authorize ERs as ITMOs and apply an adjustment, including for voluntary markets. Compliance-based carbon crediting program Carbon credit programs established for compliance with laws or international agreements. These can be domestic, as is the case for compliance with regulatory carbon pricing instruments, or international, as is the case for compliance with NDCs or the Carbon Offsetting & Reduction Scheme for International Aviation (CORSIA). Double counting A situation where the same mitigation outcome is counted more than once toward a mitigation target (e.g., two countries using the same ITMOs toward their NDC achievement under the Paris Agreement). Emissions reduction GHG abatement resulting from activities that are carried out to reduce greenhouse gas emissions from sources. Emissions removal GHG abatement resulting from activities that remove greenhouse gases from the atmosphere and store it in geological, terrestrial, or ocean reservoirs, or in products. ERC financing Financial capital provided to ERC activities or to ERC project developers. Internationally transferred mitigation outcomes (ITMOs) Article 6.2 of the Paris Agreement allows for the authorization and transfer of ITMOs, i.e., real, verified, and additional emissions reductions and removals generated from 2021 onward and transferred between countries for use towards their NDC commitments and for other international mitigation purposes. This latter category encompasses both ‘international mitigation purposes’ (e.g., use towards an international compliance obligation such as CORSIA and “other purposes as determined by the first transferring participating Party” (also known as ‘other purposes,’ which some interpret as a reference to the voluntary carbon market or VCM). Methodology Technical blueprint for ERC activity design and the quantitative measurement of mitigation outcomes achieved. Other international mitigation purposes ITMOs can also be authorized and transferred for use towards ‘other international mitigation purposes,’ which encompasses both ‘international mitigation purposes’ (e.g., use towards an international compliance obligation such as the Carbon Offsetting and Reduction Scheme for International Aviation or CORSIA) and 'other purposes as determined by the first transferring participating Party' (also known as ‘other purposes,’ which some interpret as a reference to the voluntary carbon market or VCM). Party A country which is a signatory to an international agreement such as the UNFCCC or the Paris Agreement. Footnote 1: Adapted from World Bank, State and Trends of Carbon Pricing 2022. There may be some overlap between crediting mechanisms and between market segments due to the heterogenous interaction between the different carbon markets.

Key ERC-related terms

This section is intended to be a living document and will be reviewed at regular intervals. The Guidelines have not been prepared with any specific transaction in mind and are meant to serve only as general guidance. It is therefore critical that the Guidelines be reviewed and adapted for specific transactions. Unless expressly stated otherwise, the findings, interpretations, and conclusions expressed in the Materials in this Site are those of the various authors of the Materials and are not necessarily those of The World Bank Group, its member institutions, or their respective Boards of Executive Directors or member countries. For feedback on the content of this section of the website or suggestions for links or materials that could be included, please contact the PPPLRC at ppp@worldbank.org.

Updated: April 5, 2024

TABLE OF CONTENTS

UNLOCKING GLOBAL EMISSION REDUCTION CREDIT

Introduction to Emission Reduction Credits

Strategic Guidance for Country System Assessments

Guidance for Countries in Assessing ERC Projects

Related Content

Additional Resources

Climate Toolkits

Page Specific DisclaimerFind more at Climate-Smart PPPs or Download the Full Report and its sector-specific toolkits for Roads, Renewables, Hydropower, ICT and Water Production and Treatment.

KeywordsClimate & Disaster Risk Screening Tools

PPP Reference Guide