Overview of Assets Recycling Through Islamic Finance

Photo Credit: Image by Pixabay

On this page: Find details of Islamic Finance in Assets Recycling below, or visit the Guidelines for Implementing Asset Recycling Transactions Section Overview and Content Outline, or Download Full Report for more.

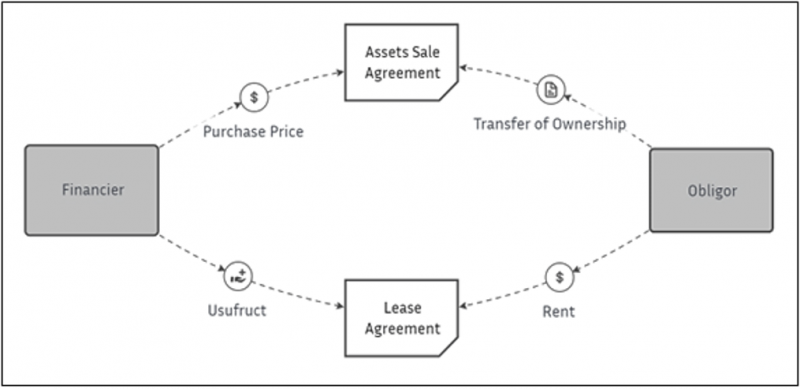

One strikingly common feature between assets recycling and Islamic finance is that both are primarily based on assets. In asset recycling, revenue generating public assets are identified for monetization purposes and then monetized proceeds are invested in new or existing infrastructure assets. Similarly, Islamic finance is an asset-based and risk-sharing financing technique and money in Islamic finance generally does not move without the movement (in the form of transfer of ownership or usufruct) of certain underlying assets. Accordingly, Islamic finance appears to be a natural fit for assets recycling transactions. Unlike loan based conventional financing techniques, Islamic finance is asset based and generally involves: (a) an equity-based / sharing-based structure, e.g., musharakah (partnership) and mudarabah (partnership in profit); (b) a sale based structure, e.g., murabahah (sale with profit), istisna'a (build / manufacture) and salam (advance purchase); (c) a lease-based structure, e.g., ijarah (leasing); or (d) a fee-based structure, e.g., wakalah (agency), kafalah (guarantee) and ju’alah (service contract). Given a typical asset recycling transaction would involve transferring the control of an asset capable of generating income in exchange for financial consideration, the Islamic finance instruments most suitable to facilitate such transfer for assets recycling purposes are considered to be various forms of lease (ijarah) based structures including: (a) sale and leaseback, (b) long-term lease and short-term lease (head lease and sub-lease); and (c) asset-backed sukuk al-ijarah. Sale and leaseback Ijarah or lease is the transfer of the usufruct of an asset to another person in exchange for a rent claimed from that person. The leased asset must have a usufruct, or a legal right to use and derive profit or benefit from the assets. In order to be Shari'ah compliant, an ijarah must be transparent, detailed and the terms agreed prior to execution. The lessor under an ijarah must maintain legal and beneficial ownership of the asset and bear responsibility for risks associated with ownership of the asset. In other words, there must be a link between a financier's ability to earn profits and the assumption of risk. In a sale and leaseback arrangement the obligor sells certain specified assets that it owns to the financiers for an agreed price and then the obligor (as lessee) takes the same assets back on lease from the financiers (as lessor). The result is an immediate cash inflow for the obligor (in the form of sale price of the assets). In the context of an assets recycling financing, the obligor (typically a government) will ring-fence the sale price and invest it in new or existing infrastructure assets. The obligor continues to use the assets in lieu of periodic rental payment to the financiers who now owns the assets. An ijarah arrangement must comply with all of the following general Shari'ah requirements applicable to a lease: In the context of Islamic finance, the form of ijarah typically used is known as an ijarah wa iqtina (i.e., a lease-and-purchase transaction or buy-back leasing). This form of ijarah includes a promise by the financiers as lessor to transfer the ownership of the leased asset to the obligor, as lessee, either at the end of the lease period or in stages during the term of the ijarah. An ijarah wa iqtina is essentially the Islamic equivalent of a conventional equipment lease contract outlined in the diagram below. The lessee is responsible for all ordinary maintenance (other than major maintenance); typically repair, replacement and maintenance of the assets, for example, basic wear and tear. In addition, the financiers will be responsible for the insurance of the assets and payment of ownership related taxes. To limit the financiers' liabilities and to ensure that third parties do not have any claims on the financiers or its assets, the obligor and the financiers enter into a service agency agreement pursuant to which the obligor is appointed as agent of the financiers for the purpose of carrying out the major maintenance, procuring the insurance and paying the ownership related taxes. If the obligor fails to effect any repairs or replacements, or obtain insurance, the financiers may do so and will be indemnified by the obligor for all amounts paid or costs incurred by the financiers. If the obligor is found negligent in the use or maintenance of the assets, or in procuring insurance or performing any of its obligations listed under the service agency agreement, it assumes principal liability for and will be required to indemnify the financiers for any related losses. A sale and leaseback structure typically incorporates purchase undertaking (put option) and sale undertaking (call option) arrangements following termination or expiry of the lease. Pursuant to the terms of the sale undertaking, the financiers usually undertake to sell all or part of the assets to the obligor in the event of a partial or full cancellation or prepayment of the facility and following the discharge by the obligor of all outstanding payments owed to the financiers. If the obligor defaults, the financiers normally have the benefit of a purchase undertaking (put option) from the obligor. This is a form of acceleration of the facility. Upon occurrence of a default, if the financiers exercise their rights under the purchase undertaking, the obligor is obliged to purchase the leased assets for a purchase price equal to the aggregate of amounts outstanding under the facility. The documentation normally stipulates that title to the assets does not pass to the obligor until the amounts owed to the financiers have been discharged in full. However, by exercising the purchase undertaking the financiers will have a claim against the obligor for an amount that is immediately due and payable and will thus have a claim in the proceeds of any security package available in relation to the financing. In an ijarah-based financing, a total loss of the underlying leased assets (that is, if the assets are destroyed, damaged beyond repair or otherwise completely lost) will have a major impact on the leasing arrangements. Pursuant to Shari'ah principles, a lease arrangement will be terminated with immediate effect upon the occurrence of a total loss of the leased assets (i.e., the underlying assets) and any purchase undertaking with respect to those assets becomes ineffective as a result. In order to mitigate this risk, the financiers typically appoint the obligor as their service agent under a service agency agreement and require it, in such capacity, to maintain insurance with respect to the full replacement value of the leased assets. Upon the occurrence of a total loss, the obligor (as service agent) will be under an obligation, within a given timeframe, to provide the financiers with the proceeds of the insurance. In the event that the proceeds are less than the full replacement value of the assets, the obligor will have failed to comply with its strict insurance obligations (as service agent) under the service agency agreement and will be liable to indemnify the financiers for any shortfall. In light of the above, the process of a sale and leaseback structure can be summarised as follows: This structure was used in 2014 when the government of Pakistan adopted a sale and leaseback structure with the Lahore Motorway (located in Islamabad) being the underlying asset. The sale proceeds of the underlying assets were directed towards the State Bank of Pakistan whereby it was used to reduce domestic debt. Similarly, in the Ras Al Khaimah sukuk, a sale and leaseback structure was adopted involving a road owned by the government of Ras Al Khaimah. The issuer was a Cayman Islands-incorporated company independent from the government. While a sale and lease based structure is widely accepted by Shari'ah scholars for Islamic finance transactions, we are aware that some Shari'ah scholars and Islamic finance institutions consider a sale and lease back structure as a less preferred option for structuring an Islamic finance transaction. Long-term lease and short-term lease (head lease and sub-lease) Under a long-term lease and short-term lease (head lease and sub-lease) arrangement, instead of entering into an assets sale agreement the obligor and the financiers enter into a long-term (for example 99 or 49 years) lease agreement pursuant to which the obligor leases the underlying assets to the financiers for a longer period. In turn, the financiers enter into to a short-term lease agreement pursuant to which the financiers lease the assets back to the obligor for a period during the tenor of the financing. All other aspects including other related transaction documents (i.e., service agency agreement, purchase undertaking and sale undertaking) are expected to be identical as explained under sale and leaseback structure above. For instance, in Bahrain, a head-lease-sublease structure was adopted allowing the Bahraini government to lease certain vacant land at Bahrain International Airport to the obligor, a Bahraini company established by the Central Bank of Bahrain for the purposes of the transaction, for 100 years. Sukuk al-ijarah While sukuk are often referred to as "Islamic bonds", they are more akin to Islamic trust certificates, representing an undivided beneficial ownership interest in an underlying asset wherein the return is based on the performance of that underlying asset. The assets themselves may be tangible or intangible provided that they are certain, income-generating and not being used for any non-Shari'ah compliant purposes such as gambling or the sale of alcohol. The salient features of sukuk are that they are generally asset-based securities, and any profit or benefit derived from the sukuk is linked to the performance of a real asset and the risks associated with the ownership of that asset. Sukuk are therefore distinguishable from conventional bonds, which are bearer negotiable debt securities that pay the holder fixed or floating interest on a periodic basis during the term of the bond. However, sukuk have certain common features with conventional bonds, such as being freely transferrable on the secondary market if the sukuk is listed, paying a regular return, and being redeemable at maturity. Sukuk therefore have to be linked to an underlying asset (using, for example, an ijarah arrangement) to generate revenues that mirror the coupon payments received under a conventional bond. The return generated is justified as the certificate-holder has an ownership interest in the underlying asset as represented by the sukuk and is thus assuming ownership risks. The Bahrain based Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI) has identified 14 eligible types of sukuk, of which sukuk al-ijarah and sukuk al-murabahah are the most common. Of these alternatives, sukuk al-ijarah is considered to be the most appropriate structure for asset recycling purposes. A sukuk al-ijarah includes two Islamic finance techniques, namely sale and ijarah. The basic structure and mechanics for an assets sale agreement and a lease agreement in a sukuk al-ijarah is the same as described under paragraph (a) above in the context of a sale and leaseback financing structure. The Islamic finance industry generally regards sukuk al-ijarah as the classical sukuk structure and it has become the most commonly used structure for issuing sukuk. This structure's popularity stems from its uncontested Shari'ah-compliance and investors' familiarity with the sale and leaseback structure. To structure a sukuk al-ijarah, the obligor needs to have encumbered assets that are commercially leasable (for example, real estate). The rental payments payable to sukukholders can be either fixed or calculated with reference to a market rate, such as Term SOFR. Sukuk al-ijarah involves the transfer of ownership or benefit/usufruct of tangible assets (such as real estate), from an originator to a special purpose vehicle ("SPV"), which then issues to investors sukuk certificates representing undivided ownership interests in such assets. The asset is then leased back to the originator by the SPV for a specified term, which is typically commensurate with the term of the certificates. Each sukukholder is entitled to receive the rentals generated under the lease pro rata to its ownership interest in the underlying sukuk assets. The amount of these rentals is equal to, and used by the SPV to pay, the periodic distribution amount payable under the sukuk at the relevant time. This amount therefore may be calculated by reference to a fixed rate or variable rate (e.g. Term SOFR) depending on the type of sukuk issued. On the issuance date, the originator will enter into a purchase undertaking which gives the right to the SPV to oblige the originator to purchase the assets following a sukuk dissolution event or on scheduled maturity, at an exercise price equal to the principal amount plus any accrued but unpaid periodic distribution amounts. The money received by the SPV will be used to pay the dissolution amount due to investors under the sukuk. A sukuk al-ijarah structure may consist of the following steps: Sukuk al-ijarah can be categorized into asset-backed and asset-based structure. Although sukuk is generally issued by an orphan SPV, typically the investor will not be bearing an exposure solely to the credit risk of that SPV. Most sukuk transactions in the current sukuk market are primarily intended to allow the investors to be exposed to the credit risk of the obligor. Sukuk may however be structured as such that investors will not have any recourse to the obligor rather their recourse will be to the segregated and ring-fenced underlying sukuk assets. The connection between the funding arrangement and the underlying sukuk assets to which it relates is fundamental to understand the economic risk of the sukuk and its risk allocation. Whether (a) the investors will have legal recourse to the underlying sukuk assets (what is generally referred to as an asset-backed sukuk) or (b) the investors only have recourse against the obligor because that transfer of the underlying sukuk assets is not as effective against third parties or the insolvency estate of the obligor (what is generally referred to as an asset-based sukuk) will depend on whether the sukuk assets underlying the funding arrangement has been permanently transferred to the SPV. In asset-backed sukuk, there is a real (true) sale and absolute transfer of the underlying sukuk assets to the third party which is an SPV. The SPV acts as a trustee or agent (as relevant) on behalf of sukukholders and collects rental from the lessee of the assets and transfer the same to the sukukholders. The SPV collects money as the issuer of the sukuk and manages the assets, whereas, the ownership of the assets will belong to the sukukholders. Since underlying assets will be separated from the book of originator, there would not be recourse to the obligor. It should be noted that, for asset-backed sukuk to be acceptable from Shari'ah perspective, the underlying assets must be free from any dispute or legal issues, must not have obstacle that void the real transfer of the assets from the obligor to the SPV who act as a trustee or agent (as relevant) on behalf of the sukukholders and must generate cash flow from the underlying assets. Sukukholders own the underlying sukuk assets under an asset-backed sukuk structure and therefore do not have recourse to the obligor if there is a deficit in payment. On the contrary, the sukukholders do not have the right of ownership of the underlying assets under the asset-based sukuk. If there is a deficit in the payment, the sukukholders have recourse to the obligor not underlying assets as the sukukholders are generally beneficial ownership not legal owner of the underlying assets. Beneficial ownership has rights of the property that belong to a person despite the legitimate title of the assets belongs to someone else. Hence, in such situation, the sukukholders are only guaranteed security interest in the sukuk assets and the sukukholders are recognised as creditors and not owners of the assets. An asset-backed sukuk al-ijarah permits the holders of sukuk to liquidate the underlying assets in any case of default to recover their investments while asset-based sukuk al-ijarah only represents beneficial ownership on the underlying assets and it limits sukukholders' right in the event of default by the obligor. In an asset-based sukuk structure, the overriding reliance of the investors is on the credit strength of the obligor rather than the underlying sukuk assets. In an asset-backed sukuk, on the contrary, the return of capital and profit is ultimately based on the underlying sukuk assets themselves. Unlike in an asset-based structure, the investors can be expected to want to try to assess the value of the assets (and the related underlying transaction) themselves. While most sukuk transactions in the current sukuk market are asset-based, for an assets recycling transaction, asset-backed sukuk al-ijarah structure appears to be more relevant. However, that does not mean that an asset-backed structure will always be more appealing to investors rather that would depend on the credit strength of the obligor compared against the value of the underlying assets. Generally, when the sukuk assets are seen to be more bankable than the credit strength of the obligor, investors will prefer asset-backed structures. It is considered that Islamic finance and ESG (environmental, social and governance) investing are complementary investment approaches sharing significant common ground, such as being a good steward to the society and the environment. Both offer products that appeal to Shari'ah-compliant and non-Shari'ah-compliant investors alike, and hold strong practices and policies that each can learn from the other. There is growing awareness among global investors of the synergy between ESG investing and Islamic finance, contributing to the rising appetite for Shari'ah-compliant investments as investors look for greater portfolio diversification and an alternative to more traditional ESG investments. Sukuk by their nature are ethical as they cannot be used to finance impermissible activities and they are structured to avoid high degrees of leverage and speculation. Shari'ah compliancy prohibits speculation and demands high levels of transparency, meaning the outcome of transactions must not be entirely dependent on chance and all rights and obligations relating to an investment must be clear. A green sukuk is a sukuk that is issued to finance assets that benefit the environment, such as renewable energy projects. There are several types of green sukuk, including sovereign (issued by a government) and corporate (issued by a private sector organisation). Green sukuk are Shari’ah compliant investments in renewable energy and other environmental assets. They address Shari'ah concern for protecting the environment. Green sukuk is considered a form of ethical, inclusive and socially responsible finance, because it connects the financial sector with the real economy and promotes risk sharing, partnership style financing, and social responsibility. Green sukuk could be an innovative way of financing green infrastructure. It has the potential to become a new asset class targeting both Islamic and socially responsible investors. Eligible assets for green sukuk may include solar parks, biogas plants, wind energy, ambitious energy efficiency, renewable transmission and infrastructure, electric vehicles and infrastructure and light rail. The other aspects of an assets recycling through green sukuk will follow the normal course of an assets recycling transaction. That is to say a government can ring-fence the sukuk proceeds collected from the investors in exchange the investors' share in the profit generated from the green assets. Such government can then apply the ring-fenced sukuk proceeds in new or existing infrastructure projects. Murabahah based Islamic finance structure could generally be sued for almost all circumstances including for an assets recycling transaction. Murabahah is a form of sale where the seller explicitly informs the purchaser of the cost price of acquiring the assets in addition to the seller's profit or mark-up on that cost price. Murabahah is valid only where the exact cost of the assets can be ascertained. If the exact cost cannot be ascertained, the assets cannot be sold on murabahah basis. The profit in a murabahah can be determined by mutual consent of the parties, either in lump sum or through an agreed ratio of profit to be charged over the cost. All the expenses incurred by the seller in acquiring the assets (like freight, custom duty or tax) are included in the cost price and the mark-up is applied on the aggregate cost price. A widely used variation of the murabahah contract is the tawarruq (monetization) structure. Under a tawarruq structure, following the obligor's acquisition of the assets (generally commodities traded on the London Metal Exchange) from the financiers, the obligor appoints an agent (usually one of the financiers, who acts as agent of the financiers in relation to the financing) to sell the same assets to a third party and thereby receives cash.Introduction to Islamic Finance instruments for assets recycling

In the context of an assets recycling financing, the obligor (as lessee) and the financiers (as lessor) will enter into a lease agreement to lease the identified underlying assets immediately after signing the assets sale agreement. Pursuant to the lease agreement, the obligor will lease the assets from the financiers in return for lease payments.

The lease payments could be fixed or variable. In the case of a variable lease, rental payments are calculated by aggregating: (a) a fixed element, equivalent to principal on the conventional facilities; (b) a variable element, generally on the basis of a reference such as six-month Term SOFR, plus a fixed fee, which is equivalent to the applicable margin under the conventional facilities; and (c) a service amount, which is equivalent to the amount paid to the obligor, in its capacity as service agent under the service agency agreement, (further explained below) by the financiers. Lease payments can be structured to be made at the same times as equivalent payments under conventional facilities.

In accordance with Shari'ah principles, unlike in conventional operating leases, the financiers (in their capacity as owners of the assets or lessors) are responsible for all major maintenance; typically repair, replacement and maintenance without which the assets could not reasonably be used by the lessee.

Sukuk – asset-backed and asset-based

Green sukuk as an asset class for assets recycling

Other structured Islamic Finance products

Islamic Finance product suitability analysis

Islamic finance product

Sale and leaseback

Long-term lease and short-term lease (head lease and sub-lease)

Sukuk al-ijarah

An equity-based / sharing-based structure e.g., musharakah

A sale based structure) e.g., murabahah

A lease-based structure e.g., ijarah

A fee-based structure e.g., wakalah

Can this product be used to facilitate funding via asset recycling?

Yes

Yes

Yes

Yes

Yes

Yes

Not independently

Can this product be used to transfer the control of an asset?

Limited transfer (unless a true sale happens)

Limited transfer

Limited transfer

Limited transfer

Full transfer

Limited transfer

Limited transfer

What is the level of risk for the obligor (the government)?

Low

Mid

Mid

High

Low

Mid

High

What is the level of risk for the financier?

Mid

Low

Low

High

High

Low

Low

Market appetite for this product

Mid

Low

High

Mid

High

Mid

Low

How complex is this product?

To an extent

Complex

Complex

To an extent

Not complex

Not complex

Not complex

Is this product Shari'ah compliant?

Yes (however some Shari'ah scholars / institutions may have some reservations about this structure)

Yes (however some Shari'ah scholars / institutions may have some reservations about this structure)

Yes

Yes

Yes (however some Shari'ah scholars / institutions may have some reservations about this structure)

Yes

Yes

Overall Suitability for Asset Recycling

Suitable

Suitable

Very suitable

Not suitable

Suitable

Suitable

Not suitable

The Guidelines have not been prepared with any specific transaction in mind and are meant to serve only as general guidance. It is therefore critical that the Guidelines be reviewed and adapted for specific transactions To find more, visit the Guidelines to Implementing Asset Recycling Transactions Section Overview and Content Outline, or Download the Full Report.

![]()

Updated:

TABLE OF CONTENTS

I. GUIDELINES FOR IMPLEMENTING ASSET RECYCLING

7. Bundling and Unbundling Criteria

8. Climate Finance in Asset Recycling

9. Islamic Finance and Asset Recycling

• Introduction: Islamic Finance in Asset Recycling

• Key Considerations of Islamic Finance in Assets Recycling

• Overview of Assets Recycling Through Islamic Finance

• Assets Recycling Process in Islamic Finance

• Case Studies on Islamic Finance for Asset Recycling

• Way Forward for Countries to Tap Into Asset Recycling Through Islamic Finance

Related Content

Additional Resources

Financing and Risk Mitigation

Type of ResourceProject Finance – Key Concepts

Type of Resource